Congrats on the Gig, Kevin Warsh. You’re Cooked.

He wanted to win the Fed chairmanship so badly. But what did he actually win?

IN ECONOMICS, THERE’S A CONCEPT called the “winner’s curse.” It means that the person who ends up winning an auction has often overpaid for the prize. It’s a good way of characterizing the fate of the newly confirmed Federal Reserve chair, Kevin Warsh.

Warsh has been auditioning to lead the Fed for over a decade now, muscling out competitors and massaging his public image. The main way Warsh finally got the gig was by pledging to cut interest rates, which was Donald Trump’s litmus test. Unfortunately for Warsh, he will not be able to deliver on that promise for reasons that are clear to everyone except, perhaps, Trump. This means that Warsh is hurtling toward a reckoning with his benefactor.

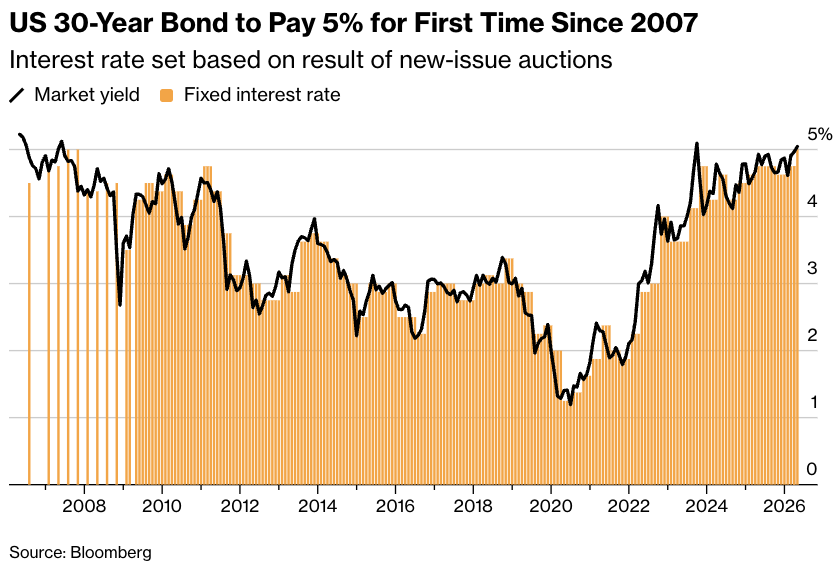

This is all related to the scary little chart right here:

Yesterday, for the first time since 2007, rates on new 30-year Treasury bonds surpassed 5 percent. And look, I realize that was possibly the most boring sentence you will read today.1 So let me explain what it means, why it matters to the economy, and why it suggests Warsh is very, very cooked.

IT STARTS WITH TRUMP’S economic policy agenda.

Inflation had been drifting downward in recent years, at least roughly until “Liberation Day” in April 2025 when Trump announced global tariffs. The rate of price growth soon started ticking back upward.

Then the Iran war happened. And, as was evident in new reports this week on consumer and producer prices, inflation has been supercharged. With consumer prices reaching 3.8 percent growth in April from a year earlier, we’re likely seeing only the earliest glimmers of the war’s effects on prices for energy, food, manufactured goods, and so forth.

Even worse, this one-two punch of tariffs and war threatens to reset expectations for how bad inflation will get. What this means is that instead of these shocks being temporary (dare I say “transitory”), we could be at the start of a vicious cycle in which companies that are fearful of getting surprised by higher prices in the future raise their own prices preemptively today. If everybody does this at once, you get more inflation. It’s a self-fulfilling prophecy.

Companies and consumers aren’t the only ones who worry about inflation. Anyone who lends to the government worries about it, too: They don’t want the interest they receive on those loans to get eaten up by inflation. They want to make money!

This brings us to the infamous 30-year bonds. This week, there was an auction for Treasuries, which are the debt instruments the U.S. government sells so it can pay its bills. And buyers demanded higher interest rates on that government debt as compensation for the very real risk that inflation will run higher for a while. They demanded it both for shorter-term Treasuries and longer-term ones, as well. That’s why you saw 30-year bonds selling at their highest yield in nearly two decades.

If those bonds stay around 5 percent (or higher), a few things can happen.

First, obviously, is that the debt load the government carries becomes more expensive. U.S. debt was already on an unsustainable path, given how much we spend vs. how much we collect in tax revenue. Higher interest rates make carrying that debt even more painful. The government already spends about as much on interest as it does on Medicare. If you’re worried about a fiscal doomsday clock, things like this bring us a few ticks closer to midnight.

Second is that financial conditions for the rest of the economy will remain tight.

Rates for mortgages, business loans, credit cards, car payments, and similar are all sensitive to what happens to rates for government debt. To be clear, most of the time, private debt rates are not mechanically pegged to the rate for a specific Treasury instrument. But in practice, they’re closely related, since Treasuries are supposed to be the safest, least-risky form of debt out there. Everything else gets benchmarked against them.

The more expensive it is to finance a home or a car, the angrier voters will be. This, in turn, will also make Trump mad. And all of this will hem in the Fed, which looks less credible if it’s slashing interest rates while markets are freaking out about inflation.

San Diego here we come! We’re thrilled to announce our lineup for this Bulwark Live featuring special guest San Diego Mayor TODD GLORIA. Plus our very own MAGA culture expert WILL SOMMER.

Join Sam, Tim, and Sarah for this one-night live show at the Balboa Theatre on May 20. Grab your seats today.

THIS BRINGS US to Warsh’s quandary. Warsh has said he intended to cut interest rates (specifically, the short-term rates that the Fed has the most control over). But with inflation rising, that objective is increasingly undesirable, or impossible—or both.

Markets have already communicated this: They don’t currently expect any additional cuts through at least the end of 2027. If anything, rate hikes are more likely, particularly next year.

And regardless of what markets are communicating, Warsh himself is primed to believe we need higher rates, too. He is widely known as an inflation hawk2—someone whose concerns about inflation push them to err more on the side of higher interest rates than making risky cuts.

But let’s assume he nonetheless still wants to deliver the rate cuts Trump expects. Guess what? He can’t.

For starters, Warsh will be only one of twelve votes on the Fed committee that sets interest rates, and the rest of the committee is making it clear they’re not interested in more cuts. So Warsh has no good options here.

He could try to convince the rest of the committee to cut rates. But he will almost certainly fail.3

Alternatively, he could watch everyone else vote to keep rates steady (or to raise them), and be a lone vote for cuts. That is, he could throw the rest of the Fed officials under the bus and proclaim to Trump that he really, really wanted to deliver rate cuts, but no one else would cooperate.

I cannot overstate how cuckoo that would be.

The chair’s job, for decades, has been to build consensus. Most of the time, the twelve-person voting committee votes unanimously, with the policy decision more or less pre-negotiated by the chair in advance. There are occasional dissents,4 but the idea of an open dissent by the sitting Fed chair is almost unheard of. The last time it happened was 1939.

Today, it would signal a significant breakdown in leadership. Warsh would look at best ineffectual, and at worst like the sockpuppet Democrats accused him of being when he refused to answer who won the 2020 election. It would be an act of self-humiliation.

There is another option. Warsh could vote like the hawk that he is in his heart. He could put his name down for either steady or higher interest rates alongside his Fed colleagues. But in that case, he’d face Trump’s wrath—and, possibly, the same type of smears, threats of (illegal) termination, and bogus criminal investigations that Trump has flung not only at Warsh’s predecessor, Jerome Powell, but also at his fellow Fed governor Lisa Cook. For all we know, Trump’s henchman and housing appointee Bill Pulte has already begun amassing an oppo dossier on Warsh in preparation for precisely this scenario.5

If that were to happen, at least Warsh would have someone there to guide him through it. Cook remains on the Fed, awaiting a Supreme Court decision about her fate (though Pulte has recently insisted that if he can get an indictment against her it would prove legally sufficient to fire her from the post). Powell persists on the Fed Board, as well; he chose to stay on after his chairmanship ended as a bulwark for institutional independence. Perhaps just in case, ahem, anyone else at the bank goes wobbly.

Maybe Warsh thinks he can manage Trump. Maybe he thinks his marriage to the daughter of a close Trump ally6 will shield him from the full force of Trump’s rage and retribution. But other onetime confidants with even closer ties to MAGA’s paterfamilias have been shredded for less.

Congrats on your new gig, Mr. Chairman. Good luck to you.

Ramparts

— The Goodyear tire plant in Fayetteville, North Carolina announced that it will close in 2027; roughly 1,700 people will lose their jobs.

— Perhaps another indicator of a softening labor market: Some big companies are cutting back on their paid leave policies. At one time there was something of an arms race, at least in the tech industry, to provide better and better fringe benefits, including family-related benefits (also fertility benefits, backup childcare, and much else). As the AI-pocalypse comes for tech and other professional services, we may see some of those benefits disappear.

— Speaking of victims of AI: Princeton just chucked its 133-year-old tradition of not proctoring exams and relying solely on a quaint notion called “students’ honor.” The reason: the sordid temptations of Claude.

— And speaking of the victims of AI and college students: The job market sucks for new grads. Or maybe for young people of all educational attainment levels? And why is it seemingly worse here in the States? New Gallup polling finds the United States is one of the few countries where younger workers are more pessimistic about their finances than older workers are; in fact we have the “largest gap of any country in job market perceptions between younger and older adults.”

Even I hear the phrase “long bonds” in a Ben Stein monotone.

At least when he’s not auditioning for Fed chair.

Unless we have a major recession, which could make the Fed more amenable to rate cuts. But it really depends on how bad inflation is at that point, and whether inflation or unemployment is the bigger problem. This is why stagflation sucks so much: Inflation suggests higher rates are needed, while stagnation/recession/unemployment suggests lower rates are needed. That’s when the Fed gets most stuck.

More common lately than for most of Fed history.

Warsh is a centimillionaire who appears in the Epstein files. Even if he’s squeaky clean—as I presume he is—a motivated DOJ could likely still launch a bogus but costly criminal investigation into him on something. Who knows what kind of seashell patterns he traipsed by in St. Barts?

Cosmetics magnate and Greenland conquistador Ronald Lauder.

The "winner's curse" was succinctly described nearly 60 years ago in the Star Trek episode "Amok Time", when Spock tells his romantic rival Stonn, "After a time, you may find that 'having' is not so pleasing a thing, after all, as 'wanting'. It is not logical, but it is often true."

Yep, my thoughts exactly. Kevin, you have made your bed in hell. Your term will be an unending browbeating to lower interest rates. If you try to emulate Powell, and refuse, you may find yourself "under investigation" on some manufactured bogus charge. If you cave, you became the betrayer to your own principles. And the self-hatred that act will conjure. I don't see how your turn as Fed chair will go well for you personally or professionally. But ambition is a never enough satisfied need for many people.